|

|

|

|

|

TOKYO, July 24, 2017 - (JCN Newswire) - Showa Denko ("SDK"; TSE:4004) hereby announces revised forecasts of consolidated financial results for the first half of 2017 and full-year 2017. SDK announced the earlier forecasts on April 25, 2017, and decided this time to revise them, taking the recent business trends into consideration. SDK also announces that its board of directors decided today to record losses (a non-operating cost and an extraordinary loss) concerning P.T. Indonesia Chemical Alumina (ICA), to which equity method is applied.

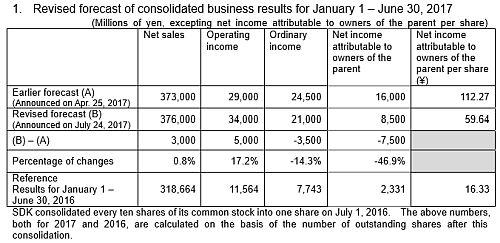

1. Revised forecast of consolidated business results for January 1 - June 30, 2017

Table 1: https://www.acnnewswire.com/topimg/Low_sdk17072401.jpg

Reasons for the revision of consolidated performance forecast

Net sales will be at the same level as the earlier forecast. Operating income in the Petrochemicals segment is expected to exceed the earlier forecast because a strong market continues, reflecting the tight supply-demand balance in the Asian market. Operating income in the Electronics segment will exceed the earlier forecast because shipment volumes of HD media remain strong. Operating income in the Chemicals and Inorganics segments will also exceed the earlier forecast.

Though the operating income is expected to exceed the earlier forecast, ordinary income will be lower than the earlier forecast due to the recording of a loss of about 10 billion yen on investment to ICA, which is under the application of the equity method.

Net income attributable to owners of the parent will be lower than the earlier forecast due to the recording of an extraordinary loss of about 6.7 billion yen concerning ICA.

2. Recording of a loss concerning companies under the application of equity method (non-operating cost, extraordinary loss)

ICA, in which SDK holds a 20% stake, operates an alumina plant located in Tayan District, West Kalimantan, Indonesia. Recently, SDK has been discussing about the way to manage the plant of ICA in the future with ANTAM, which is the parent company of ICA. However, there is still a great difference between the shareholders' opinions on new terms and conditions to revive ICA. Thus SDK judged it is difficult for the two parties to reach an agreement on this matter in the future.

In consideration of these circumstances, at the meeting of the Board of Directors held today, SDK decided to report, in its financial statements for the second quarter of 2017, a loss on investment to companies under the application of equity method (non-operating cost) with regard to ICA, and an extraordinary loss on the whole amount of SDK's surety obligations and long term loans to ICA at the end of June 2017. SDK also decided to start negotiations with ANTAM and/or third party for the sale of the whole shares of ICA that SDK holds now.

Table 2: https://www.acnnewswire.com/topimg/Low_sdk17072402.jpg

Outline of P.T. Indonesia Chemical Alumina

(1) Company name: P.T. Indonesia Chemical Alumina

(2) Locations: Head office: Jakarta, Indonesia; Plant: Tayan District, West Kalimantan, Indonesia

(3) Representative: President, Anas Safriatna

(4) Capital: US$188,500 thousand

(5) Shareholders: PT ANTAM (Persero) Tbk (80%); Showa Denko K.K. (20%)

(6) Establishment: February 2007

(7) Products: Alumina and aluminum hydroxide

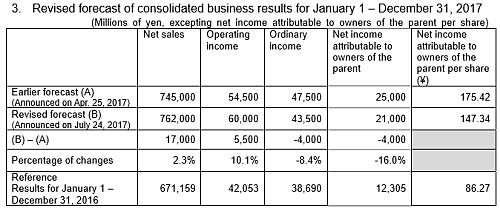

3. Revised forecast of consolidated business results for January 1 - December 31, 2017

Table 3: https://www.acnnewswire.com/topimg/Low_sdk17072403.jpg

Reasons for the revision of consolidated performance forecast

Net sales in the Petrochemicals segment will exceed the earlier forecast because actual market prices of petrochemical products in the first half of the year were higher than those assumed in the earlier forecast. In the Electronics segment, shipment volumes of HD media remain strong. As a result, overall net sales are expected to exceed the earlier forecast.

Operating income in the Petrochemicals segment is expected to exceed the earlier forecast because the spread of petrochemical products exceeded the earlier forecast especially in the first half of the year. Operating income in the Electronics segment will exceed the earlier forecast as the full-year shipment volumes of HD media are expected to be higher than the earlier forecast. Operating income in the Inorganics segment will also increase because the supply-demand balance of graphite electrodes in the Asian market is expected to become tighter.

Ordinary income will be lower than the earlier forecast because the Company has decided to report, in its financial statements for the second quarter of 2017, a loss on investment to companies under the application of equity method with regard to ICA, though operating income is expected to exceed the earlier forecast.

Net income attributable to owners of the parent is expected to be lower than the earlier forecast due partly to the Company's decision to report an extraordinary loss with regard to ICA in its financial statements for the second quarter of 2017, in addition to the expected reporting of ordinary income lower than the earlier forecast.

The revised forecast stated above is based on the assumption that the exchange rate and the domestic naphtha price will be 105 yen/$ and 38,000 yen/KL for the second half of 2017, respectively.

There is no change in the forecast of paying dividends of 30 yen per share.

Note: The above forecasts are based on the information available as of today and assumptions as of today regarding risk factors that could affect our future performance. Actual results may differ materially from the forecasts due to a variety of risk factors, including, but not limited to, the economic conditions, costs of naphtha and other raw materials, demand for our products, market conditions, and foreign exchange rates.

The above forecasts do not include the effect of planned integration of graphite electrode businesses of SDK and SGL GE, which we announced in October 2016, because the date of business integration has not been specified yet as of today.

Full Press Release (PDF): www.sdk.co.jp/assets/files/english/news/2017/20170724_sdknewsrelease_e.pdf

Contact:

IR Office, Finance & Accounting Department

Phone: 81-3-5470-3323

Topic: Earnings

Source: Showa Denko K.K.

Sectors: Chemicals, Spec.Chem

https://www.acnnewswire.com

From the Asia Corporate News Network

Copyright © 2024 ACN Newswire. All rights reserved. A division of Asia Corporate News Network.

|

|

|

|

|

|

|

|